Social Security versus Dividends in Retirement

October 31, 2019 4:11 amThe Social Security Administration (SSA) has recently announced that benefit payments in 2020 will increase 1.6% from 2019’s level.

While in one sense that’s good news, in another it is just a continuation of governmental policy that fails to deliver for seniors.

Certainly, an increase is better for seniors than no increase. But, if we look at a case study of a worker who retired in 1985, we can see that we could have done better still.

In 1985, according to the Social Security Bulletin, published June 1986/Vol. 49, No. 6, a newly retired worker received an average monthly benefit of $445. That, of course, equaled an annual benefit of $5,340 ($445 x 12).

In 1985, the dividend return of the S&P 500 was 5.82% (total return that year was 32.16%). If our hypothetical worker had $91,675 invested in the S&P 500 at the start of the year, he/she would have received $5,340 in dividends, equal to the average Social Security benefit.

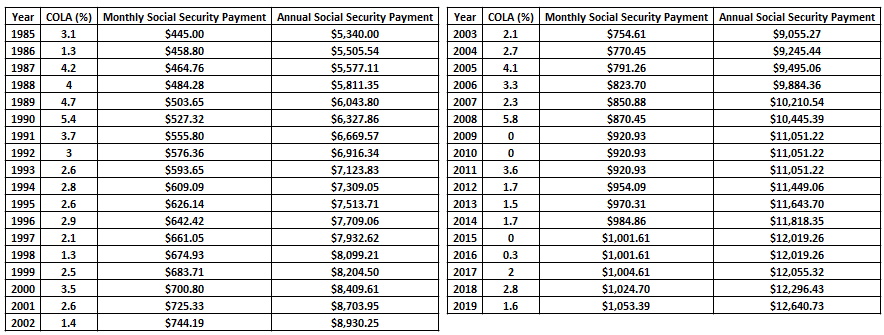

A retiree’s Social Security payment increases as the legislated cost-of-living-adjustment tied to the CPI-W is applied. We took the average 1985 payment and increased it each year by the COLA to produce an estimate of our retiree’s payment history. The COLA increases and benefit payment were as follows, calculated from the Social Security Administration’s COLA data.

Social Security Cost-Of-Living Adjustments & Payments

Summing those annual payments, our retiree would have received $315,559 over the course of a retirement 35 years long.

But what about that money invested in the stock market over all those years?

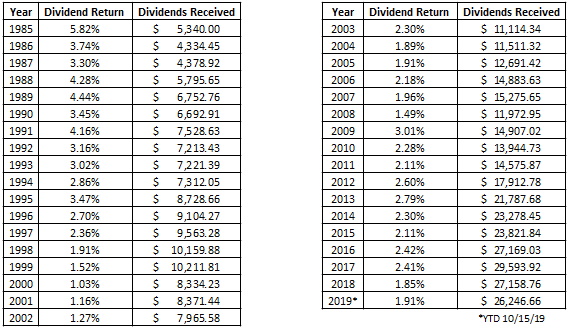

For the purposes of this discussion, we’re going to make two assumptions. The first is that we will ignore taxes for both the retiree’s Social Security payments as well as the dividend payments. And secondly, we will assume that the retiree takes and spends only the dividends received from the stock market portfolio, not the principal. Using the dividend return to the stock market each year, here’s what the retiree’s dividend stream would have been under those assumptions.

S&P 500 Dividends – Returns and $ Received

The dividends received over the years would have totaled $452,855. That’s $137,296, or 44%, more than the Social Security payments.

You might object that companies sometimes cut their dividends so it’s risky to rely on dividend payments for income.

This is true, and you can see in the table above that dividends received dropped in a number of years (2019 doesn’t count because the data is only for a partial year). But there were only six years out of thirty-five where the dividends were less than the Social Security payments. And the largest shortfall, $1,198, would have been an average difference of just $100 per month.

The elephant in the room is the value of the stock portfolio. Since the retiree was harvesting just the dividend income, the portfolio remained intact throughout retirement. From an initial value of $91,765, by the end of our period the portfolio would have grown to $1,642,133! With Social Security, there is no “principal value” to pass on to your heirs.

A logical question is where the initial $91,675 needed to invest in the stock market might come from. That’s beyond the scope of this exercise, but here’s an interesting observation. In 1985, there were just over 2 million new Social Security benefit awards to retirees and disabled individuals. To fund the $91,675 required to provide the $5,340 benefit from dividends would have required a little less than $190 billion. The federal budget in fiscal 1985 was $959 billion and in fiscal 1986 $973 billion (Budget of the United States Government, Fiscal Year 1986, Office of Management and Budget). So, $190 billion would have been very meaningful. However, using our example, if we make the improbable assumption that all of those new retirees survived fifteen years through 1999, the expenditures made by the government via their Social Security payments would have totaled even more: $211 billion. It could be that a policy transitioning from the current system to a market based system might be possible.

In any case, this study highlights the power of dividend investing, something that should be an important part of most everyone’s retirement portfolio plan.

Post from: Insights